How to Make Zero Based Budget for Personal Finances

Discover how to create a zero based budget to take control of your personal finances. Learn to track spending, improve your habits, prevent overspending, and achieve your financial goals effectively.

How to Create a Simple, Flexible , and Practical Zero-Based Budget

What Is Zero Based Budgeting

Zero based budgeting is a method where you assign every dollar of income to a specific purpose until your remaining balance equals zero. If you earn $5000 dollars, you plan for all $5000. The goal is not to spend it all. The goal is to plan it all.

This means every dollar has a job, nothing floats, nothing is extra, and nothing is left unassigned. Savings, debt payments, sinking funds, groceries, utilities, fun money, and long term goals all get a place in the plan. You choose what matters most, and your budget reflects those choices.

Unlike traditional budgeting, which often copies last month’s numbers, zero based budgeting starts from zero. You do not assume that last month’s spending was correct. You question, adjust, and realign every period. This fresh start is what makes the method so powerful.

Why Zero Based Budgeting Works for Real People

People love zero based budgeting because it brings structure without suffocating you. It is flexible enough to adapt to real life, but firm enough to keep you grounded.

It removes autopilot. Traditional budgeting assumes last month was fine. Zero based budgeting asks whether your spending still reflects your real life.

It exposes waste. Unused subscriptions, inflated grocery spending, forgotten memberships, and quiet leaks become visible.

It aligns your money with your values. You choose what matters most each month. Your budget becomes a reflection of your life, not your habits.

It supports debt payoff. Because every dollar counts, you can direct extra money toward debt snowballs or sinking funds with intention.

It adapts to fluctuating income. If your income changes month to month, this method adjusts with you.

It works beautifully with digital tools. Whether you prefer a Google Sheets budget, a printable worksheet, or an app, the structure is simple and universal.

Zero Based Budgeting vs Traditional Budgeting

Traditional budgeting.

Traditional budgeting starts with last month’s spending and simply adjusts it. If you spent a certain amount on groceries, subscriptions, or eating out last month, you usually copy those numbers into the new month with small changes. It is familiar and easy, but it also keeps old habits alive. You might continue paying for things you no longer use or spending money in ways that no longer match your current priorities. Traditional budgeting is comfortable, but it does not challenge you to rethink anything.

Zero based budgeting

Zero based budgeting starts fresh every single month. Instead of copying last month’s numbers, you begin at zero and decide what your money needs to do right now. Every dollar gets a purpose. Nothing is automatic. Nothing is assumed. You look at your real life, your real goals, and your real needs, and you build your plan from the ground up. This method encourages intention, awareness, and accountability. It helps you stop drifting and start directing.

When I finally realized I needed to pay closer attention to my financial situation, the first thing I did was create a simple budget. I wanted to see where my money was actually going instead of guessing or hoping things would work out. That first step opened my eyes. I could finally see the patterns, the leaks, and the habits that were quietly draining my income.

I started using zero based budgeting. I committed to it for about four months, and it completely changed the way I looked at my money. Instead of letting old habits decide for me, I began assigning every dollar a purpose. It felt intentional, grounding, and surprisingly empowering.

Later on, I shifted into a pay yourself first approach, but those months of zero based budgeting were the turning point. They taught me how to be aware, how to be honest with myself, and how to build a plan that actually supported my goals instead of working against them.

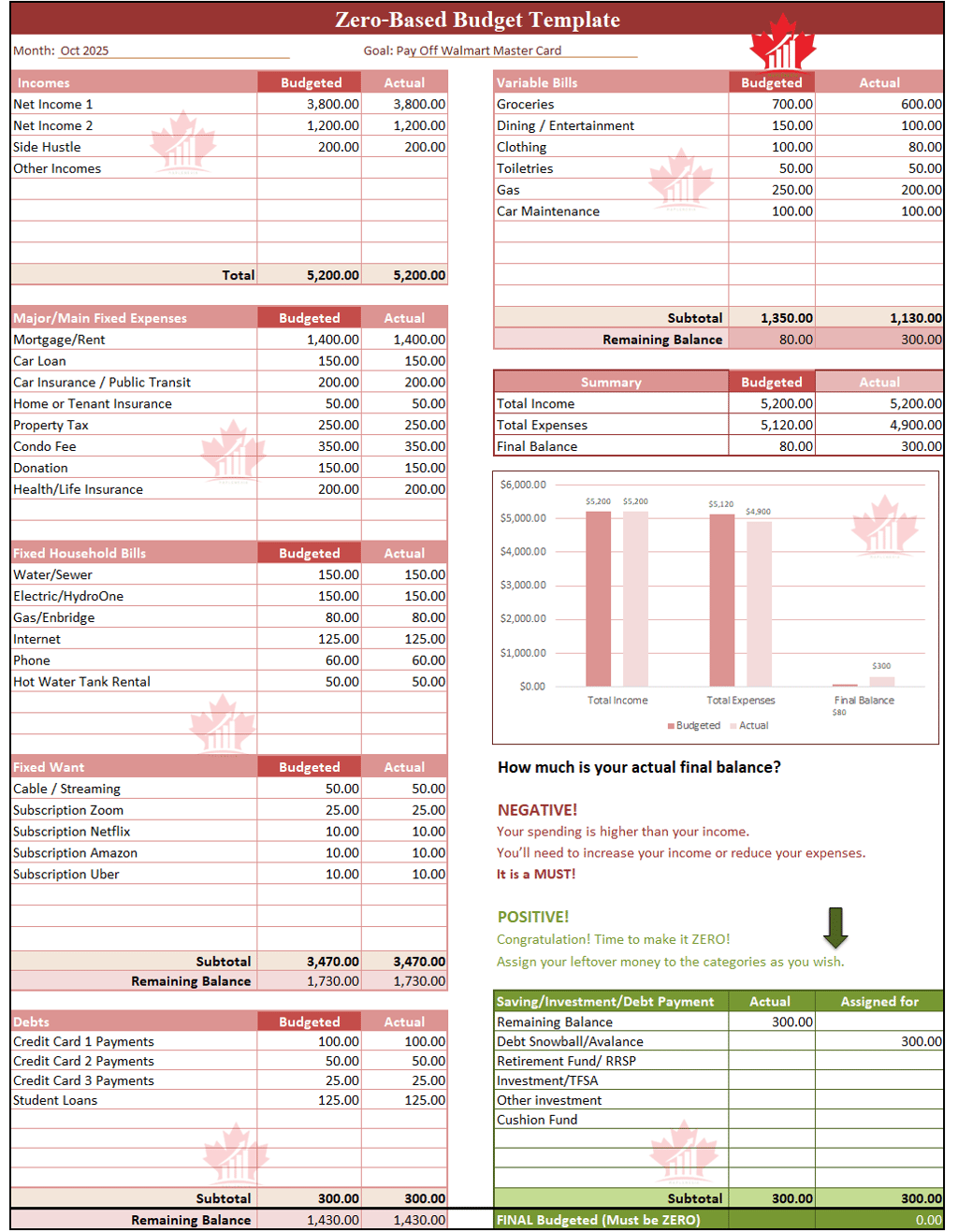

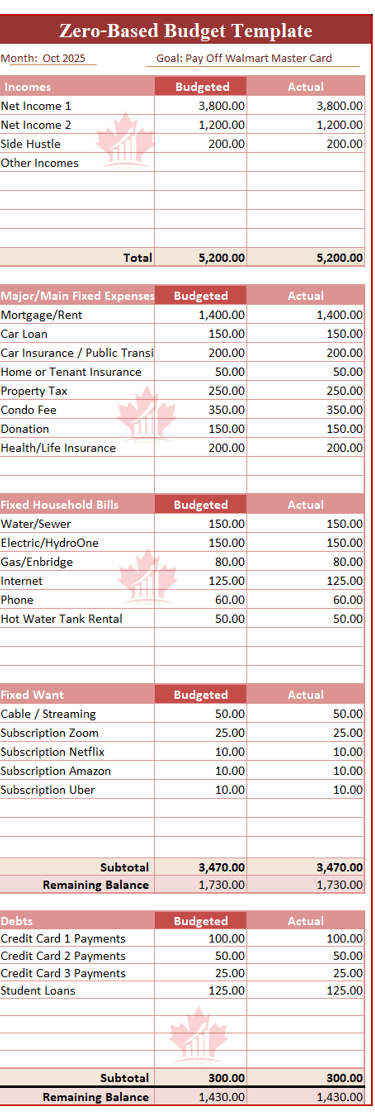

How to Create a Zero Based Budget

You can use a notebook, a printable worksheet, or a Google Sheets budget. The structure below blends clarity with flexibility, making it ideal for beginners and seasoned budgeters alike. I created my zero based budget , using a Google Sheet, you can use it!

Step 1: Set Your Goal First

No matter what budgeting method you use, the very first step is always the same: choose your goal. Zero based budgeting starts here too. Here are examples of budgeting goals:

Pay off credit card debt. Paying down high‑interest credit card balances is one of the most common financial goals.

Build an emergency fund. Many people aim to save enough to cover 3–6 months of expenses.

Save for a down payment on a home. Saving for a house is a major long‑term goal for many families.

Save for travel or vacations. Short‑term goals often include saving for trips or experiences.

Save for retirement. Long‑term planning often includes building retirement savings over time.

Step 2: List All Income

Start by writing down every source of income you expect for the month. Include your salary, side income, support payments, and small business income if you have it. If your income changes from month to month, use the lowest amount you can reasonably expect so your plan stays safe and realistic. If you are paid every two weeks, base your monthly plan on two paychecks and treat the two extra paychecks each year as bonus opportunities for savings or debt payoff - this is what I did

Step 3: Assign Every Dollar to a Category

This is where zero based budgeting becomes powerful. You divide your spending into clear sections that help you stay organized and intentional.

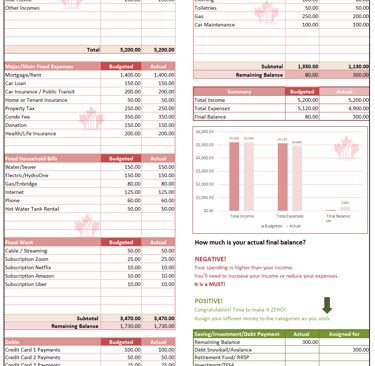

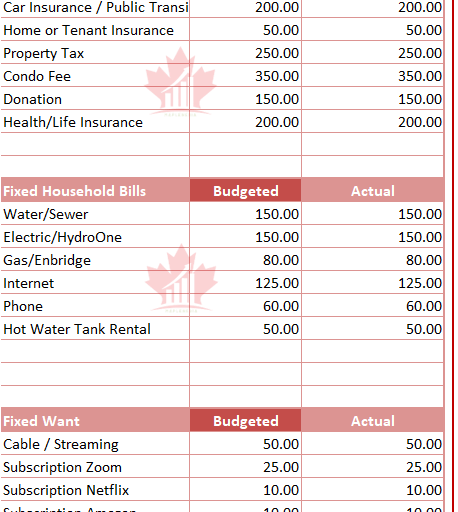

Major Expenses

This includes your major home payments such as rent, mortgage, property taxes, and home insurance. These are the foundation of your budget and usually the first items you assign. I include my regular donation budget here!

Household Basics

These are your predictable monthly utilities and home services. Include electricity, water, gas, internet, phone, and waste collection. These are the everyday essentials that keep your home running smoothly.

Debts

Here you list the minimum payments for your credit cards, student loans, personal loans, and car loans. You will add extra payments later in the savings section if you choose to.

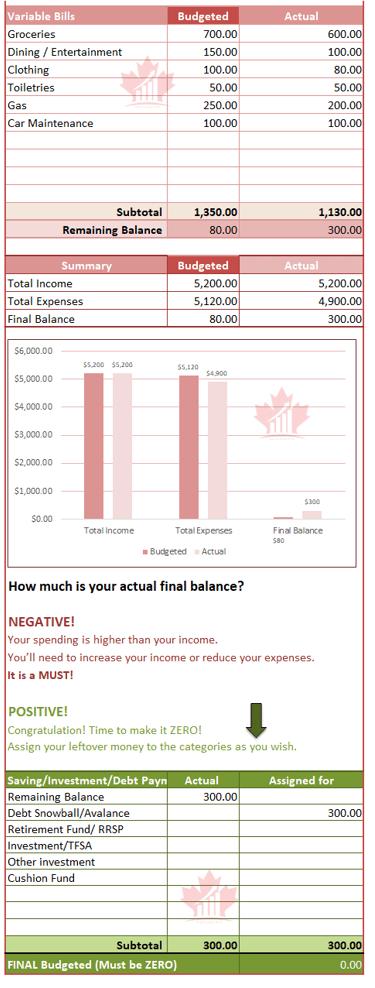

Variable Bills/Daily Living

This section covers flexible, everyday spending such as groceries, fuel, eating out, clothing, household items, and fun money.

Fixed Subscriptions

Fixed subscriptions are services you pay for every month, usually the same amount each time. These are things like Netflix, Amazon Prime, Spotify, Zoom, Canva, iCloud storage, or any app that charges you monthly. Because they renew automatically, they are easy to forget about it, remember this!

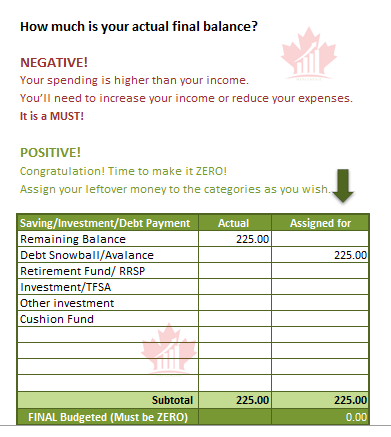

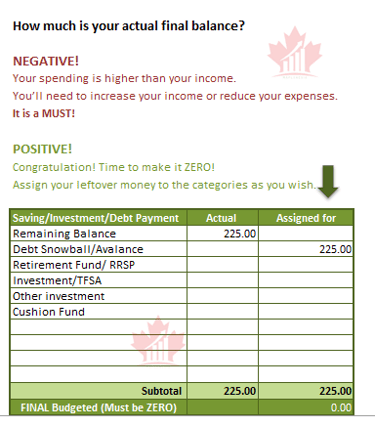

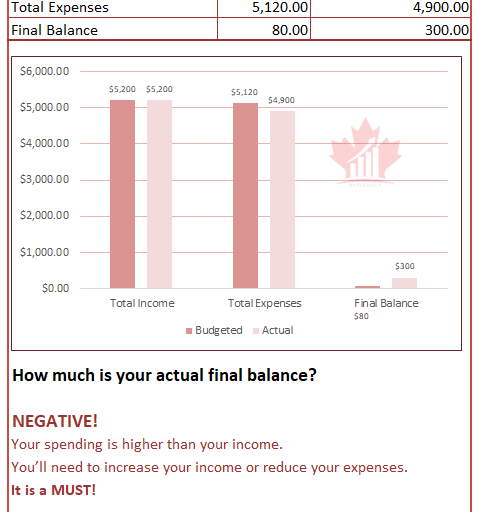

Step 4: Subtract Your Total Expenses From Your Income

If the number is negative, you need to adjust something. Either lower a few expenses or find a little extra income so your budget can work.

If the number is positive, assign it based on your goals. In zero based budgeting, that extra amount becomes the money you direct with intention. You can add it to your emergency fund, put extra toward your debt snowball, save for travel, set aside money for education, plan for home upgrades, or invest it for the future

Step 5: Monitor Your Budget Regularly

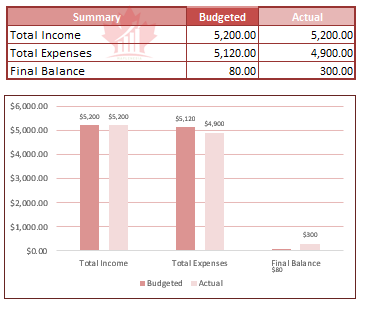

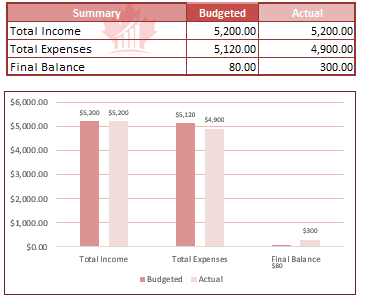

To make your budget truly work, you need to check in with it regularly. In my zero based budgeting template, there is column for your actual expenses. All is automatically calculated. By the end of the month, you’ll be able to see your real spending patterns and compare them to what you planned.

This step shows you how well you’re sticking to your budget. You’ll quickly notice which categories are over budget and which ones can be reduced — groceries, gas, and utilities are usually the first places to adjust. Tracking your spending helps you stay aware, stay honest, and stay in control.

If groceries are one of your trouble spots, you can also check out my guide on 15 ways to save money on groceries.

Step 6: Done!

Congratulations, you did it.

Now you can finally see your real spending patterns, and that awareness is powerful. Tracking your spending is essential in every budgeting system, including zero based budgeting.

From here, you can shift your habits, strengthen your budget, and choose what to do with any leftover money, whether that is saving, paying debt, or investing for your future.

Final Thoughts

Zero based budgeting is more than a financial method. It is a mindset shift. It teaches you to look at your money with fresh eyes each month, question old habits, and build a plan that reflects your real priorities.

Whether you are tackling a budget challenge, building a simple budget in Google Sheets, or trying to stretch your income further because every dollar counts, zero based budgeting gives you structure, clarity, and control.

Happy Budgeting!